Global Broker Regulation Inquiry App

About WikiFX

English

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

اردو

Dow Jones surges to a new record level as the S&P500 retreats from recent highs. Bitcoin falls below

Abstract:Key TakeawaysDow Jones outperforms as investors rotate from growth stocks into value oriented sectors.The AI-driven rally is facing a new test, with Broadcoms results triggering concerns about technol

Key Takeaways

Dow Jones outperforms as investors rotate from growth stocks into value oriented sectors.

The AI-driven rally is facing a new test, with Broadcoms results triggering concerns about technology valuations.

Asian markets remain fundamentally strong but are showing signs of exhaustion after reaching record highs.

Geopolitical developments involving the US and Iran continue to be the primary driver of short-term moves in oil and gold markets.

Crypto markets remain highly sensitive to ETF flows and leverage conditions, resulting in extreme volatility.

U.S. Markets: Dow Jones Hits New Record While Tech Rally Pauses

Commodities: Oil and Gold Swing on Iran Headlines

Cryptocurrency Market: Heavy Liquidations Hit Bitcoin and Ethereum

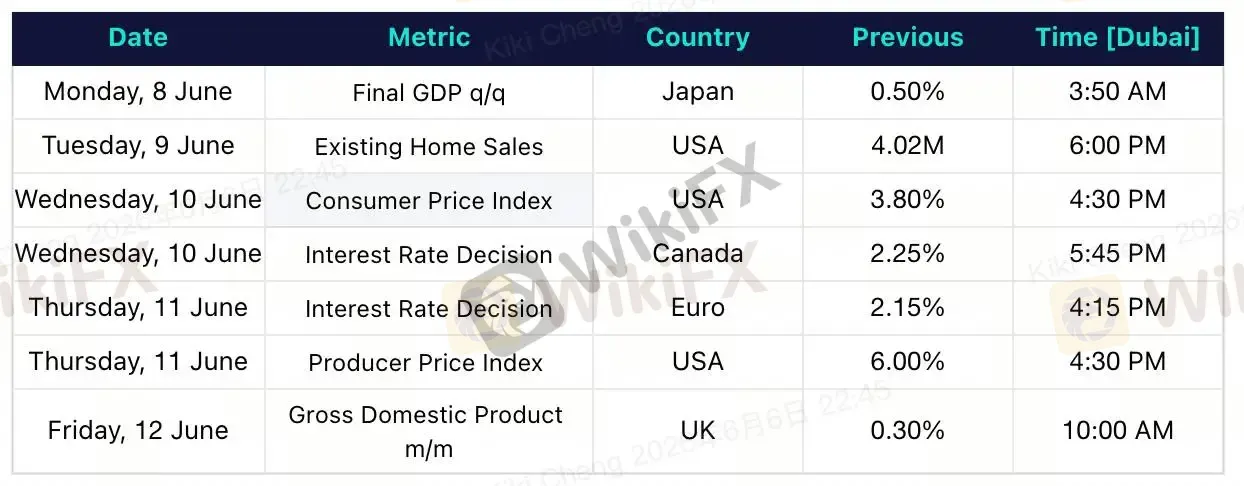

Forecast for the Week Ahead (June 8–12, 2026)

Major Economic Calendar Events for the Upcoming Week

U.S. equities delivered a mixed performance this week. The biggest highlight was the Dow Jones Industrial Average, which surged to a fresh all-time high above 51,600, supported by strong gains in financials, healthcare, and industrial stocks. Investors rotated away from high-growth technology names and into more defensive sectors amid growing concerns about AI valuations and the broader economic outlook.

Meanwhile, the S&P 500 and Nasdaq Composite retreated from their recent record highs. The pullback was largely driven by weakness in semiconductor stocks following disappointing guidance from Broadcom. Broadcom shares fell more than 12%, triggering a broader selloff across the AI-related technology sector and raising questions about whether the extraordinary AI-driven rally can continue at the same pace. By the end of the week, the S&P 500 was around 7,545, while the Nasdaq slipped despite strength in other sectors.

Oil and gold prices remained highly volatile as traders attempted to assess conflicting signals surrounding U.S.-Iran negotiations and the broader geopolitical situation in the Middle East.

Crude oil initially found support from concerns that tensions could disrupt energy supplies passing through the Strait of Hormuz. However, reports suggesting possible progress toward de-escalation later in the week weighed on prices and limited further gains.

Gold experienced similar volatility. The precious metal benefited from safe-haven demand whenever geopolitical concerns intensified but came under pressure when optimism emerged regarding potential diplomatic progress. Gold eventually rebounded toward the end of the week as investors sought protection against uncertainty and softer U.S. dollar conditions.

The cryptocurrency market suffered one of its sharpest weekly declines of 2026. Bitcoin fell below the critical $62,000 leve. Ethereum also came under significant pressure, dropping toward the $1,700 area. More than $1.5 billion worth of leveraged long positions were liquidated across the crypto market as falling prices triggered a cascade of forced selling.

Several factors contributed to the selloff including continued outflows from U.S. spot Bitcoin ETFs, increased risk aversion due to geopolitical uncertainty, and more importantly the announcement by Strategy that it sold 32 Bitcoin between May 26 and May 31. While the sale itself was relatively small, it negatively affected market sentiment and fueled concerns about institutional conviction.

Looking ahead, markets are likely to focus on three major themes.

First, investors will closely watch upcoming U.S. inflation data (CPI and PPI) for clues regarding the next moves from the Federal Reserve. Any signs of slowing growth could increase expectations for future rate cuts and support risk assets.

Second, the technology sector may remain under scrutiny following Broadcoms disappointing outlook. Investors will look for confirmation that AI spending remains strong across the broader semiconductor industry before pushing the Nasdaq to new highs again.

Third, geopolitical developments involving Iran will continue to influence oil, gold, and overall market sentiment. Any signs of de-escalation could pressure safe-haven assets while supporting equities, whereas renewed tensions may trigger another round of volatility.

For cryptocurrencies, Bitcoins ability to reclaim and hold above the $62,000 level will be critical. Failure to do so could lead to further liquidations, while stabilization in ETF flows may help restore confidence and attract buyers back into the market.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Managing False Breakouts: How to Spot and Trade the Liquidity Sweep Trap

WikiFX

WikiFXRoboForex Review 2026: Regulatory Warnings and Withdrawal Red Flags

WikiFXLONG ASIA Review 2026: Unverified Regulation and Withdrawal Risks

WikiFXYen Drops Past 163 On Oil

WikiFXUS Charges Two Over Alleged $43M Laundering Network

WikiFXSix Arrested in ₹2.68Cr Dubai-Linked Scam on Ex-IAF Officer

WikiFXHow to Tell if a Market Reversal at Support is Real

WikiFXBeirman Capital Review 2026: Unregulated Status and Key Risk Signals

WikiFXWhy the rupee keeps sliding despite RBI's $675bn arsenal

WikiFXSix Arrested in ₹20 Million Dubai-Linked Investment Scam

WikiFX