Abstract:In recent months, much debate has been about rising debt and increasing deficit levels in the U.S. F

In recent months, much debate has been about rising debt and increasing deficit levels in the U.S. For example, here is a recent headline from CNBC:

The articles author suggests that U.S. federal deficits are ballooning, with spending surging due to the combined impact of tax cuts, expansive stimulus, and entitlement expenditures. Of course, with institutions like Yale, Wharton, and the CBO warning that this trend has pushed interest costs to new heights, now exceeding defense outlays, concerns about domestic solvency are rising. Even prominent figures in the media, from Larry Summers to Ray Dalio, argue that drastic action is urgently needed, otherwise another is imminent.

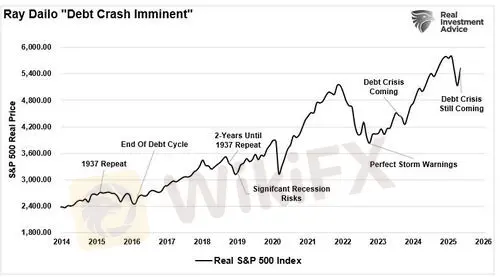

The problem with Larry Summers‘, Ray Dalio’s, and many others warnings of impending financial doom is that they have been warning of that very problem for decades. Such was the point of our previous discussion:

Here is the Problemfor Investors

For investors who listened to Dalios predictions of a coming “depression” a decade ago, they missed participating in one of the most significant bull markets in U.S. history.

Yet over the past 40 years, the national debt has grown exponentially, with none of the dire consequences repeatedly predicted. Interest rates have fluctuated, political gridlock has persisted, and deficits have widened, but the U.S. economy continues to function, grow, and attract global capital. The reason is that the U.S. continues to enjoy what economists call the of being the issuer of the worlds reserve currency. Treasuries remain the deepest, most liquid capital market globally, and the dollar is central to global trade, investment, and reserves. This creates a structural advantage that allows the U.S. to run larger deficits than other nations without facing the same level of market discipline. So long as global trust in U.S. institutions and the rule of law remains intact, there is a deep and steady demand for U.S. debt, providing a long runway before any severe funding stress emerges.

Moreover, deficit spending is no longer a temporary tool used in times of crisis; it has become an embedded feature of the economy. Social Security, Medicare, defense, and other entitlements are politically sacrosanct. At the same time, fiscal transfers are now a regular part of household consumption and corporate support. In many ways, the U.S. economy is now structurally reliant on deficit-financed stimulus. Growth, consumer spending, and even corporate investment increasingly depend on a steady stream of government outlays.

While U.S. debt and deficit levels are elevated, there is no imminent risk of fiscal collapse.However, it is worth examining the impact of rising debt and deficit levels on future economic prosperity.

The Real Problem With Debts and Deficits

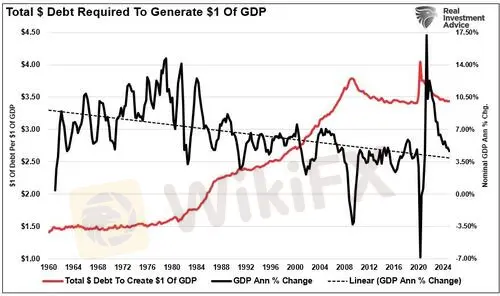

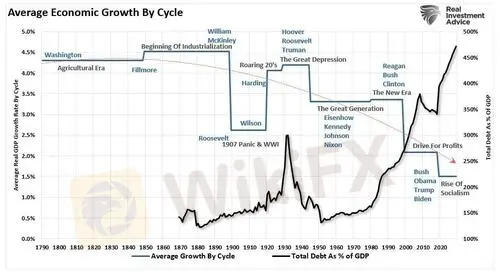

I understand the concerns about rising debt levels. However, the problem of rising debt levels for the U.S. is NOT a default but a continued degradation of economic growth. Let‘s start this discussion with a basic fact—without continued increases in debt, there would be very little to no economic growth. This is because all government debt winds up in the economy and the household’s balance sheet through lending, credit, or direct payments. We can view this by looking at the dollars of debt required to create a dollar of economic growth. Since 1980, the increase in debt has usurped the entire economic growth. The problem with the growth in debt is that it diverts tax dollars away from productive investments into debt service and social welfare.

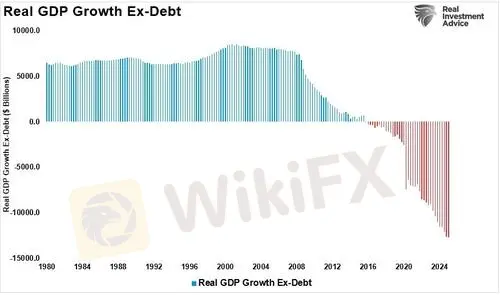

Another way to view this is to consider economic growth. In other words, without debt, there has been no organic economic growth since 2015. Thus, the debt and subsequent deficits must continue to expand to sustain economic growth.

The economic deficit has never been more significant. From 1952 to 1982, the economic surplus fostered an economic growth rate averaging roughly 8%.Today, that is no longer the case as the debt detracts from growth. Such is why the Federal Reserve has found itself in a “” where:

The problem with the current issuance of debt is that it is primarily non-productive debt.That is a crucially important concept concerning debt issuance and its impact on economic growth.

Non-Productive Debt Is The Problem

Not all debt is created equal. The key distinction lies between productiveand non-productive debt, and understanding the difference is critical to evaluating the risks and benefits of government borrowing.

Productive debt refers to borrowing used for investments that generate long-term economic returns, such as infrastructure, education, research, or business capital expenditures. These types of investments can increase future GDP, improve productivity, and ultimately pay for themselves through higher tax revenues.

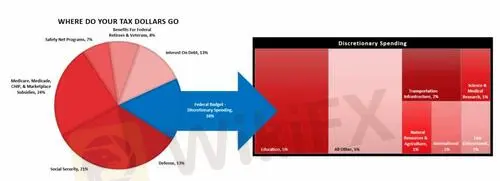

In contrast, non-productive debtfunds consumption or transfers that do not yield a measurable economic return. In the U.S., social welfare and interest payments on existing debt are a large majority of Government expenditures.

The data below shows that of every dollar spent by the Federal Government, roughly 73% is spending on social welfare and interest expense.

While the non-productive spending is necessary, primarily to support vulnerable populations, it adds to the debt burden without expanding the economy‘s capacity to grow.The U.S., like many developed economies, increasingly relies on non-productive debt to sustain economic momentum, which raises concerns about long-term fiscal sustainability. The danger isn’t the debt itself; its when borrowed funds fail to create future value, leaving future taxpayers with the bill and no corresponding economic benefit.

Dr. Woody Brocks book best explains the difference between productive and non-productive debt.

Currently, the U.S. is Country A. Increases in the national debt have long been squandered on increases in social welfare programs and, ultimately, higher debt service, which has an effective negative return on investment. Therefore, the larger the debt balance, the more economically destructive it is bydiverting increasing amounts of dollars from productive assets to debt service.

But here is where the most essential concept to understand comes into play.

A Negative Multiplier

Excess has a zero-to-negative multiplier effect, as Economists Jones and De Rugy showed in a study by the Mercatus Center at George Mason University.

Personal consumption expenditures and business investment are vital inputs into the economic equation. As such, we should not ignore the reduction of privately produced incomes. Furthermore, according to the best available evidence, the study found:

Politicians spend money based on political ideologies rather than sound economic policy. Therefore, the findings should not surprise you. The conclusion of the study is most telling.

What should not surprise you is that non-productive debt does not create economic growth. As Stuart Sparks of Deutsche Bank noted previously:

This is why the economic drag from a debt reduction would be devastating. The last time such a reversion occurred was during the

Conclusion

This is one of the primary reasons why economic growth will continue to run at lower levels. Reversing non-productive spending is impossible due to the general populations vast dependence on those programs. Reducing that spending would be “economic suicide.”

However, as noted in

While the U.S. faces a daunting fiscal outlook marked by rising debt and expanding deficits, the genuine concern is not an imminent crisis or default. Instead, the deeper, more structural issue is that an increasing share of federal borrowing is funneled into programs that support consumption but fail to generate future economic returns. That shift, which began over 50 years ago, creates a long-term drag on economic growth, crowds out private investment, and lowers the economys potential, or r*.

As the data and history show, debt to fund productive assets, like infrastructure, innovation, and education, can sustain growth and even pay for itself over time. But borrowing for entitlements and debt service does not. Unfortunately, the political and demographic realities make it nearly impossible to reverse course without severe economic fallout. Unless policymakers redirect fiscal priorities toward investment in productive capacity, the economy will remain trapped in a cycle of low growth, rising obligations, and declining returns. Innovation may offer a way out, particularly the AI-driven transformation. If leveraged wisely, with targeted investment and smart policy, AI could lift productivity, restore growth, and ease the fiscal strain.

The path forward is narrow, but not closed, and not one of imminent financial crisis. However, the real challenge will be political will.